{kind=link}

Let’s talk about HELOC rates. If you’ve had a home equity line of credit (HELOC) for a while, you likely saw your interest rate rise significantly over the past few years.

The reason is HELOCs are adjustable and tied to the prime rate, which moves in lockstep with the fed funds rate.

Since early 2022, the Federal Reserve has raised its target rate 11 times, pushing the prime rate up from 3.25% to 8.50%.

This means homeowners with HELOCs have seen their rates increase 5.25% in less than two years.

But here’s the good news; HELOC rates seemed to peak last year and the Fed has since cut rates 100 basis points (bps), providing some much-needed payment relief in the process.

There Were Three Fed Rate Cuts in 2024 After a Series of Hikes

While the financial markets are dynamic and always subject to change, data has signaled that the Fed rate hikes are done.

And even better, that more rate cuts are on the horizon between now and the end of 2025.

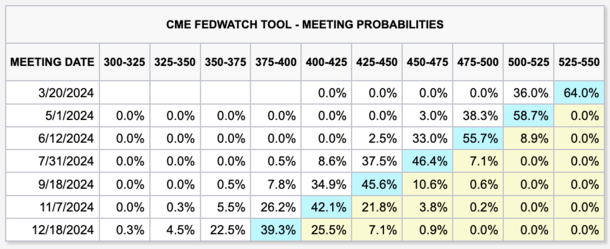

The CME FedWatch Tool, which tracks the likelihood that the Fed will change its target rate at upcoming FOMC meetings, no longer has additional rate hikes as odds-on favorites.

Instead, it has flat rates for several months until another 0.25% rate cut as the most probable move slated for the June 2025 Fed meeting.

In the meantime, rates are expected to remain unchanged, though a rate cut could arrive even sooner.

These percentage probabilities are based on interest rate trades by major brokers in the market for overnight unsecured loans between depository institutions.

The forecasts are subject to change (and do change constantly), but the data appears to be tipping more and more in favor of rate cuts instead of hikes.

In the chart above, you can see that the fed funds rate was expected to fall to a range of 3.75% to 4% by the end of 2024, but it didn’t get that low.

Instead, it reached a range of 4.25% to 4.50%, which is still down quite a bit and not terribly far from where traders expected.

And if the Fed cuts another 50 basis points in 2025, we’ll get to those predicted levels anyway.

Depending on how things pan out with the economy, a rate cut could come sooner than June, and rates could be cut more than two times this year.

The opposite is also true though, which is always the risk with an adjustable-rate loan.

HELOCs Make a Lot More Sense Than Cash Out Refinances Right Now

In recent years, home equity lending has picked up speed as interest rates on first mortgages more than doubled.

Long story short, it doesn’t make a lot of sense to apply for a cash out refinance only to lose your low fixed-rate mortgage in the process.

And the economics become less and less favorable as first mortgage rates rise.

At last glance, the 30-year fixed was averaging close to 7%, and your actual rate would likely be even higher if you elected to take cash out (why are refinance rates higher?).

This makes it a losing proposition for most, seeing that the average American homeowner has a fixed rate in the 2-4% range.

But borrowers still want to take advantage of their piles and piles of home equity and get access to cash.

The alternative is a second mortgage that doesn’t disrupt the first mortgage, but still allows for equity extraction. Options include a home equity loan or HELOC.

With a HELOC, you get the flexibility of borrowing only what you need, but the downside is an adjustable interest rate tied to the prime rate.

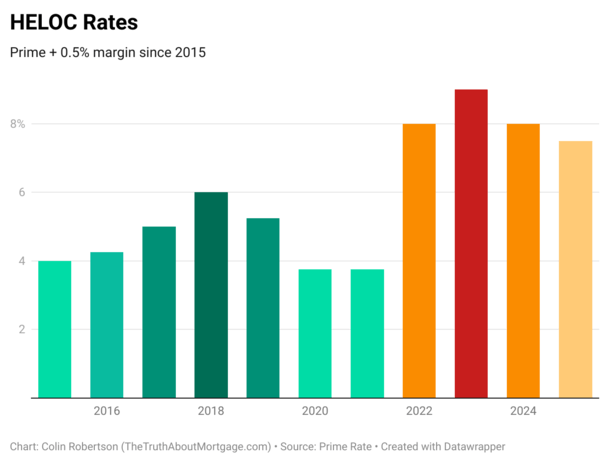

HELOC Rates Have Risen More Than 5% Since 2022

One big disadvantage to HELOCs is their variable rate. As noted, it’s tied to prime. It’s fine when prime is low and doesn’t budge.

But thanks to out of control inflation, ironically because of overly-accomodative rates, the Fed was forced to increase its own fed funds rate 11 times since early 2022.

Every time the Fed does that, the prime rate moves up by the same amount.

Currently, the prime rate is 7.50%, up from 3.25% as recently as early March of 2022.

At one point in 2023, it was as high as 8.50%, so it’s 1% below its peak and ideally heading even lower, eventually.

Imagine a homeowner who originally took out a HELOC when the prime rate was 3.25%. Perhaps their rate was prime plus .50%, or 3.50%. That’s a bargain.

But today they’d be paying an interest rate of 8% (7.50% + 0.50%) on their HELOC. Ouch!

The good news is the worst is likely behind us. But in the meantime the monthly HELOC payment is a lot higher than it used to be, especially if it’s tied to a large balance.

And chances are it is because many homeowners relied upon them to fund various home renovation projects that likely crept into the six digits.

Your HELOC Rate Depends on Prime, the Margin, and Any Discounts

The chart above shows the movement of the prime rate, which is what all HELOCs are based on.

To come up with your actual HELOC rate, a margin is added. This is basically a markup above prime that the bank takes as a profit.

So with the prime rate currently at 7.50%, you might get a rate of 8% once a 0.5% margin is factored in.

But these margins can vary widely from bank to bank, especially if you have relationship discounts as an existing customer.

For example, if you’re already a customer at the bank and use autopay, they may give you discounts of .50% to .75%.

That could push your HELOC rate down close to prime or even below for a certain period, assuming you’ve also got excellent credit and a relatively low combined loan-to-value ratio (CLTV).

Or the margin might be 1% or higher, meaning a rate of 8.50%+ on your HELOC.

Similar to first mortgages, there can be pricing adjustments on HELOCs for things like FICO score, CLTV, property type, and so on.

If you’re a very low-risk borrower with an existing relationship you should qualify for the best HELOC rates. This could land your rate at or near prime.

Learn more about how to compare HELOCs from bank to bank.

HELOC Interest Rates Could Be Another 0.5% Lower by Late 2025

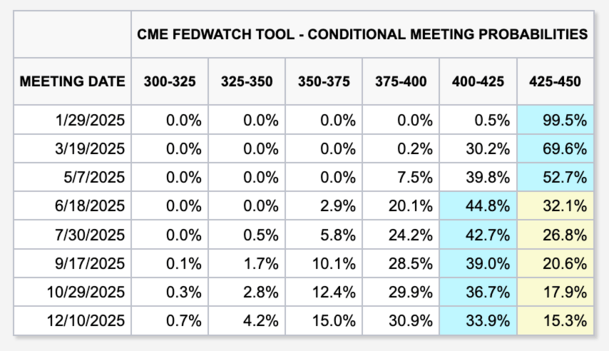

Using the CME FedWatch table from above, the fed funds rate could end 2025 in a range of 3.75% to 4.00%, which would be 0.5% below the current range of 4.25% to 4.50%.

Because the prime rate is dictated by the Fed’s hikes and cuts, that would push HELOC rates down by the same amount, so another 0.5% if these odds come to fruition.

It might not spell major relief, but it would be some relief. And monthly payments would begin falling for the many homeowners holding these adjustable-rate second mortgages.

HELOC rates are determined by combining a pre-set fixed margin and the prime rate, which we know can go up or down.

So our hypothetical borrower with a margin of 0.5% has a HELOC rate of 8%, factoring in the current prime rate of 7.50%.

If these rate cuts materialize, and the prime rate falls to 7%, they’d eventually have a rate of 7.50%.

HELOC Payments Will Fall If Prime Goes Down

If you have a HELOC, you should be rooting for a Fed rate cut. After all, it would result in a lower monthly payment and less interest due on the HELOC.

And perhaps peace of mind seeing a payment fall as opposed to rise for a change.

Rates could also keep dropping into 2025 if more rate cuts are warranted based on economic conditions.

So when shopping for a HELOC, consider the fact that rates (and payments) will likely fall over the next year.

This might sway your decision to go with a HELOC instead of a fixed-rate home equity loan instead.

One nice thing about a HELOC is the fact that you don’t have to pull out the full amount of the line initially.

You can open one and do the minimum draw if you think rates are going to be unfavorable for the foreseeable future. Then you can access more cash later once HELOC rates settle down again.

What About Mortgage Rates and Fed Rate Cuts?

While the fed funds rate does not dictate mortgage rates, it can play an indirect role.

Simply put, if the fed funds rate starts falling because the economy is slowing, it could signal lower long-term rates over time.

That would result in a lower 30-year fixed as well, as a cooler economy and lower inflation can bring down 10-year bond yields that correlate with mortgage rates.

In addition, more certainty from the Fed could result in a narrower mortgage rate spreads, which have nearly doubled in recent years.

So we might also conclude that first mortgage rates, along with HELOC rates, have already peaked too.

Of course, mortgage rates might take some time to come down and could remain “sticky” at these new higher levels.

Still, any relief is welcomed after seeing mortgage rates exceed 8% in late 2023.

While there’s a good chance we’ve already seen peak interest rates this cycle, there’s still reason to be cautious as economic data continues to flow in.

Any surprises could derail these current estimates, though they do seem to be finally moving more decisively in the right direction.

Read on: Three differences between HELOCs and home equity loans.

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the home loan process. Follow me on Twitter for hot takes.